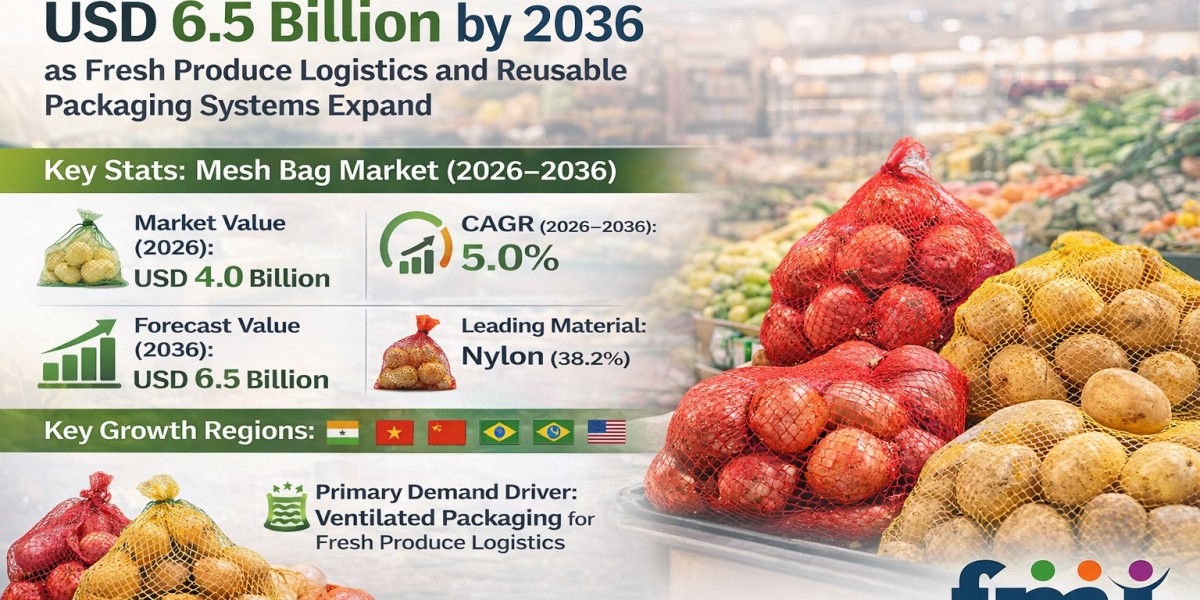

The global mesh bag market is entering a steady growth phase as agricultural supply chains, retail distribution networks, and industrial handling systems increasingly adopt breathable packaging formats designed for airflow, visibility, and operational efficiency. Valued at USD 4.0 billion in 2026, the market is projected to reach USD 6.5 billion by 2036, expanding at a CAGR of 5.0%, according to the latest analysis by Future Market Insights (FMI).

Quick Stats: Mesh Bag Market (2026–2036)

• Market Value (2026): USD 4.0 Billion

• Forecast Value (2036): USD 6.5 Billion

• CAGR: 5.0%

• Leading Material Type: Nylon (38.2%)

• Leading Application Segment: Agriculture & Produce (46.1%)

• Key Growth Regions: India, Vietnam, China, Brazil, United States

• Primary Demand Driver: Ventilated packaging for fresh produce logistics

Structural Growth Driver: Expansion of Fresh Produce Trade and Bulk Distribution

Global trade in fresh produce continues to expand, increasing the need for packaging formats that support airflow, moisture control, and visual inspection during transport and storage. Mesh bags have become a preferred solution in produce logistics due to their lightweight construction and ability to reduce condensation buildup that can damage crops.

FMI analysis indicates that as international produce exports and domestic distribution programs expand, mesh bag usage grows proportionally with logistics scale and packaging standardization.

Operational Adoption: Packaging as Part of Handling System Design

In modern distribution systems, mesh bags are treated less as standalone packaging products and more as components within handling system engineering.

Distribution operators specify ventilated mesh packaging to balance:

• Airflow and ventilation during transport

• Load stability during stacking and palletization

• Visual inspection during sorting and retail display

• Weight reduction during bulk distribution

This operational focus explains why supplier changes typically occur only during contract tenders or seasonal crop program resets.

Technology and Engineering Trends in Mesh Bag Development

Packaging engineering innovation in the mesh bag market is increasingly shaped by automation and performance validation. Key technological directions include:

• Warp-knit and woven mesh constructions optimized for airflow and load-bearing strength

• Reinforced seams and edge binding to prevent rupture during high-weight loads

• Machine-compatible closure systems including drawstrings, clips, and integrated tagging

• Lifecycle durability testing to determine reuse rotation counts

• Material consistency control for yarn strength and stitch density

As automated weighing, filling, and labeling systems become standard in packhouses and distribution centers, bag geometry and seam placement are being designed specifically to maintain high throughput and reduce machine jams.

Segment Highlights

By Material Type

• Nylon (38.2% share): Leading material due to high tensile strength, abrasion resistance, and stable performance across wet and dry logistics conditions.

• Polyethylene: Widely used where lighter loads and lower cost structures are required.

• Polypropylene: Preferred in applications requiring higher stiffness and chemical resistance.

• Cotton: Maintains niche demand in natural-material packaging programs and short reuse cycles.

By Application

• Agriculture & Produce (46.1% share): Dominant segment driven by the need for ventilation, moisture drainage, and visible product inspection.

• Retail & Consumer Goods: Focuses on presentation and lightweight product handling.

• Industrial & Construction: Requires stronger mesh structures capable of handling rough loading conditions.

Regional Outlook: Emerging Markets Driving Volume Expansion

Demand for mesh bags is expanding across both developed and emerging economies as retail supply chains modernize and reusable packaging programs gain traction.

• India (5.8% CAGR): Growth supported by expanding retail distribution networks, e-commerce logistics, and increasing adoption of reusable packaging.

• Vietnam (5.5% CAGR): Rising demand from agricultural cooperatives and fresh produce export programs.

• China (5.2% CAGR): Large-scale urban logistics and packaging programs driving adoption.

• Brazil (4.9% CAGR): Demand supported by agricultural packaging and retail supply chains.

• United States (4.3% CAGR): Mature market with stable demand across grocery and industrial packaging sectors.

Asia-Pacific remains the fastest-growing region due to expanding agricultural exports, rising urban consumption, and investments in logistics infrastructure.

Risk Landscape: Material Variability and Application-Specific Design

Despite stable demand fundamentals, the mesh bag market faces structural challenges that limit rapid standardization:

• Variability in polymer yarn supply chains and knitting methods

• Application-specific requirements across crops and industrial uses

• Long qualification timelines tied to transport and handling trials

• Limited ability to consolidate packaging SKUs across product categories

Because mesh bag structures vary significantly between applications—such as onions, citrus, firewood, or consumer goods—manufacturers must maintain multiple product formats within their portfolios.

Competitive Landscape: Performance Validation Drives Supplier Selection

The mesh bag market remains moderately fragmented, with suppliers competing primarily on material durability, reproducibility of production, and engineering support during validation trials.

Key companies operating in the global mesh bag market include:

• Knack Packaging Private Limited

• Karatzis S.A.

• Nutec Manufacturing, Inc.

• Tex-Pro Inc.

• Agribag International Ltd.

• Tufbag Industrial Co., Ltd.

• KB Poly Industries

• Vedder Industrial Ltd.

• Flexipol Packaging Limited

• Mega Plastic Industries

• Sagar Polypack

Suppliers that can deliver consistent yarn quality, scalable manufacturing capacity, and reliable dimensional control typically secure long-term supply agreements with agricultural exporters and retail packaging programs.

Outlook: Mesh Bags Become a Core Component of Produce Logistics Systems

By 2036, mesh bags are expected to remain a foundational packaging format across fresh produce logistics, retail distribution, and industrial material handling.

The market’s future growth will be anchored in four structural trends:

• Expansion of global fresh produce trade

• Adoption of reusable packaging programs

• Automation in packhouse and distribution operations

• Increasing emphasis on ventilation and moisture control in packaging

For an in-depth analysis of evolving formulation trends and to access the complete strategic outlook for the Market through 2036, visit the official report page at: https://www.futuremarketinsights.com/reports/mesh-bags-market